By Vera Wilson

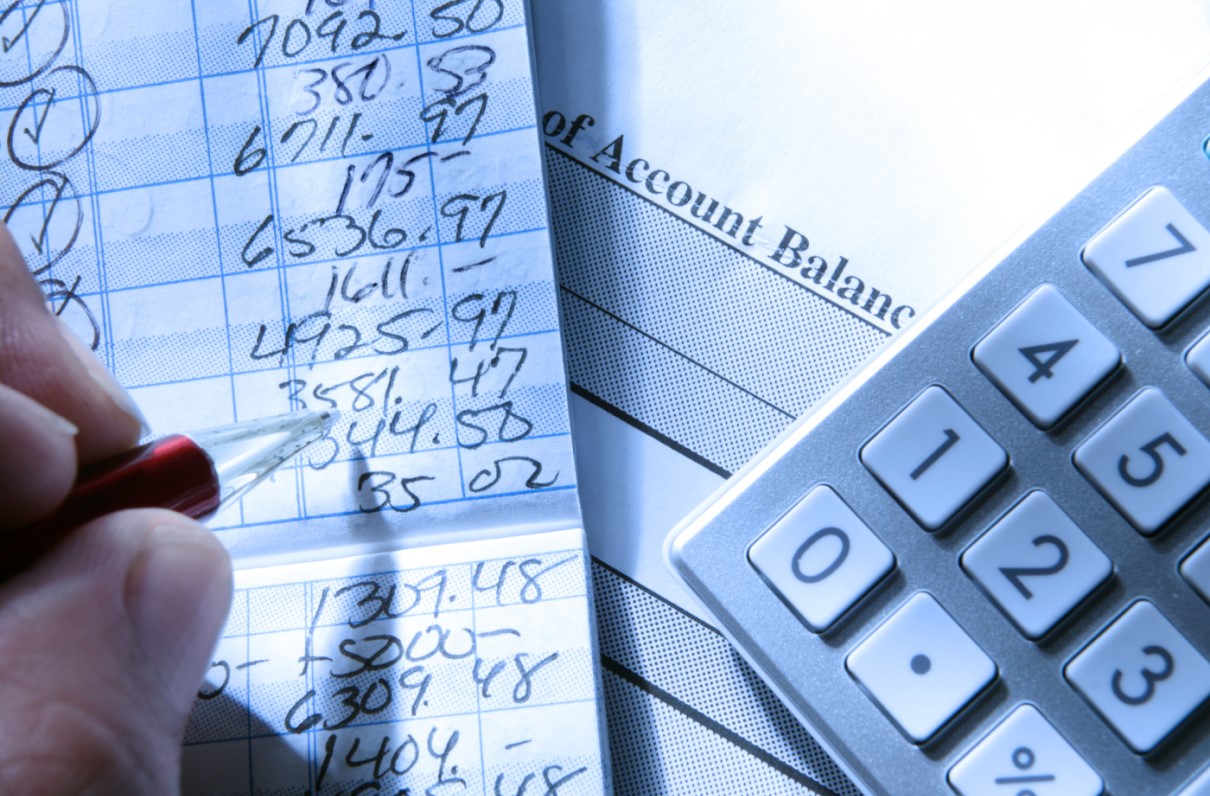

In the good old days, we used a check register -- a little booklet provided by the bank where you could record all your deposits and expense transactions so you would know (to the penny) what you had to spend.

Well, it’s 2019, and guess what? You still should be maintaining a check register.

Online banking is great, but it reflects only transactions that have been received by your bank. So if your neighbor’s daughter left for her European tour before cashing your graduation gift check, it won’t be reflected in the bank’s balance but definitely impacts the money you have available to spend. (Note: Banks can refuse checks presented six months after the check date, but they don’t have to.)

[RELATED: MOAA Life and Premium Members Can Download These Personal Finance Publications]

Even if you only use a debit card or mobile payment service, you’re not safe: Sometimes these transactions can take a couple of days to clear. Setting up automatic payments is convenient, but keep in mind, a mortgage payment scheduled to be deducted on the first of the month might take a few more days due to a holiday and/or weekend.

So the onus is on you, not the bank, to keep a running tally of all your purchases, regardless of your method of payment, as well as your deposits. Your bank will provide you a check register if you ask, but you can download and print your own. If you’re paper-averse, try an app like Checkbook-Account Tracker (for Android or iOS).

Don’t neglect to balance your checkbook, which means making sure your entries match the bank’s. (See YouTube for easy tutorials.) Bank mistakes are rare, but they might not be caught if you don’t take the time to balance your account every month.